The Hidden Fee Trap: How Companies Steal Your Money (And How to Stop Them)

The Invisible Expense Category

You budget carefully, track your spending, and think you know where every dollar goes. Then you look at your bank statement and see charges you don't recognize, services you thought you canceled, and fees that seem to appear out of nowhere.

Welcome to the world of hidden fees, one of the biggest threats to your financial independence that nobody talks about.

Hidden fees aren't accidents. They're carefully designed revenue streams that companies use to extract money from customers who aren't paying attention. The average American household pays hundreds or even thousands of dollars annually in fees they don't understand, didn't agree to, or forgot they signed up for.

Today we're going to expose the most common hidden fee traps and give you the tools to avoid them entirely.

Why Hidden Fees Are So Effective

The Psychology of Fee Avoidance

Companies have spent millions studying how to separate you from your money without you noticing:

Complexity: Buried in fine print, complex terms, or multiple fee structures

Timing: Charged after you're already committed or invested in the service

Small amounts: Individual fees seem minor, but they compound over time

Opt-out instead of opt-in: You're automatically enrolled unless you actively decline

Difficult cancellation: Making it hard to stop services you no longer want

The Compound Effect

A $9.99 "convenience fee" here, a $4.95 "processing charge" there. These might seem trivial individually, but they add up:

$15/month in various hidden fees = $180/year

$180/year invested at 7% for 30 years = $1,825

That's $1,825 of your FI money stolen through intentional complexity

Banking and Financial Services Fees

The Big Ones to Watch

Overdraft fees: Average $35 per incident, can trigger multiple times per day

ATM fees: $3-5 per transaction at out-of-network machines (plus your own bank might charge you too!)

Monthly maintenance fees: $10-25/month unless you meet minimum requirements

Wire transfer fees: $15-50 per transfer

Cashier’s check fees: $10 per check

Foreign transaction fees: 2-3% of purchases made abroad or online with foreign merchants

Defense Strategies

Choose the right bank:

Credit unions often have lower fees than big banks

Online banks typically have fewer fees than brick-and-mortar

Look for accounts with no monthly fees or easily waivable requirements

Optimize your banking behavior:

Set up low balance alerts to avoid overdrafts

Use your bank's ATM network or get fee reimbursements

Link savings to checking for overdraft protection (usually cheaper than overdraft fees)

Use credit cards for foreign purchases instead of debit cards (if the card has no foreign transaction fee)

Read the fee schedule: Every bank publishes a fee schedule. Actually read it. You might be surprised at how long the list is!

Subscription and Service Traps

The Auto-Renewal Maze

Free trial that requires credit card: "Free for 30 days" but charges automatically unless you cancel

Annual billing after monthly trial: Sign up for monthly, get charged annually

Difficult cancellation: Must call during business hours, navigate phone trees, or argue with retention specialists

Zombie subscriptions: Services you forgot about but keep paying for

Streaming and Digital Services

Content platform proliferation: Netflix, Hulu, Disney+, HBO Max, Apple TV+, Paramount+, Peacock, etc.

Average household now pays $79/month for streaming services

Easy to accumulate multiple services and forget what you're paying for

Software subscriptions: Adobe Creative Suite, Microsoft Office, various apps

Monthly charges add up quickly

Often more expensive than purchasing software outright

Difficult to track across multiple services

Gym and Club Memberships

Annual fees: Hidden in contract, charged separately from monthly dues

Initiation fees: One-time charges not mentioned in advertised prices

Impossible cancellation: Requirements to cancel in person, specific timing windows, certified letters

Automatic renewal: Contracts that auto-renew for full terms

Defense Strategies

Use virtual credit cards: Services like Privacy.com (there are others) let you create single-use or limited cards for trials

Set calendar reminders: Note trial end dates and cancellation deadlines

Use prepaid cards for trials: Prevents automatic charges when card expires

Read cancellation policies: Before signing up, understand how to cancel

Annual subscription audit: Review all recurring charges quarterly

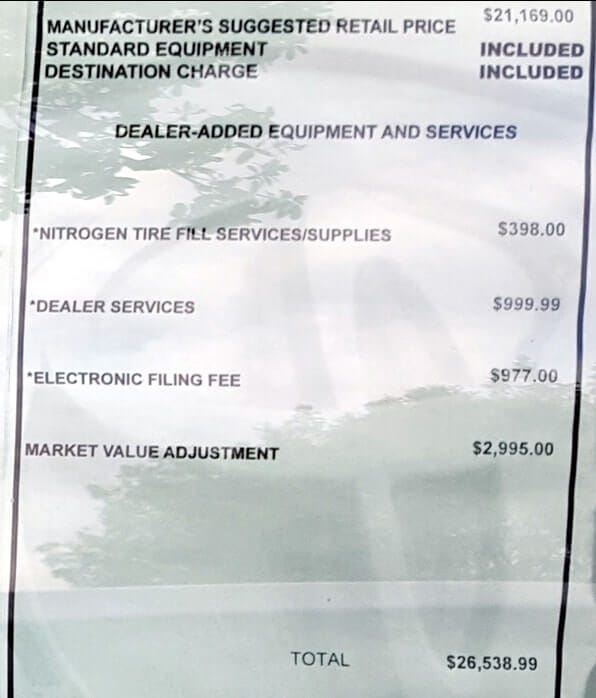

Retail and E-commerce Tricks

Online Shopping Fees

Shipping and handling: Often more expensive than actual shipping costs

Processing fees: Additional charges for credit card payments

Rush processing: Extra fees for faster fulfillment

Restocking fees: Charges for returning items

Size or weight surcharges: Additional fees for larger items

Travel and Event Booking

Booking or service fees: Ticketmaster, Expedia, and similar platforms add substantial fees at checkout

Resort fees: Hotel charges for "amenities" you can't opt out of (e.g. the wifi is free after you pay the $45/night resort fee!)

Seat selection fees: Airlines charging for advance seat selection

Baggage fees: Charges for checked or even carry-on luggage

Change and cancellation fees: High penalties for modifying travel plans

Note: I nearly always fly Frontier or Spirit, but I also do so with a single personal item and zero add-ons. As soon as you start using add-ons, it may not be worth it.

Defense Strategies

Compare total costs: Always look at final price including all fees

Book directly: Airlines, hotels, and venues often have lower fees when booking direct (and the service is better when things go wrong than going through a third party)

Read the fine print: Understand all potential charges before purchasing

Use cards with travel protections: Some credit cards reimburse travel fees

Consider alternatives: Sometimes paying more upfront costs less total (checking bags day of is usually more expensive)

Utility and Service Provider Tricks

Telecommunications

Activation fees: One-time charges for setting up service

Equipment rental: Monthly charges for modems, routers, cable boxes

Early termination fees: Penalties for canceling contracts

Upgrade fees: Charges for changing service levels

Installation and service call fees: Even for problems caused by the provider

Insurance Hidden Costs

Policy fees: Administrative charges on top of premiums

Payment processing fees: Extra charges for monthly instead of annual payments

Coverage gaps: Services you think are covered but aren't

Claim processing fees: Charges for filing claims

Defense Strategies

Own your equipment: Buy modems and routers instead of renting

Negotiate fees: Many fees are waivable if you ask

Annual payments: Often cheaper than monthly with processing fees

Read policies carefully: Understand what's covered and what isn't

Shop regularly: Don't assume renewal is your best option

Investment and Financial Product Fees

The Wealth Killers

Expense ratios: Annual fees charged by mutual funds and ETFs

Load fees: Sales charges when buying or selling mutual funds

Advisory fees: Annual percentage charges for financial advice

Trading commissions: Per-transaction charges for stock trades

Account maintenance fees: Annual charges for retirement accounts

Why These Matter Most

Investment fees compound over decades:

1% annual fee on $100,000 portfolio

After 30 years at 7% returns: $66,000 lost to fees

That's enough to retire 2-3 years earlier

Defense Strategies

Use low-cost index funds: Expense ratios under 0.1% instead of 1%+

Avoid load funds: No-load funds perform just as well without sales charges

Choose low-fee brokerages: Fidelity, Vanguard, Schwab over high-fee advisors

Understand 401(k) fees: Review plan documents and push for better options

DIY investing: Simple index fund portfolios don't require expensive advice

How to Fight Back

The Fee Audit Process

Step 1: Gather statements

Bank statements for last 3 months

Credit card statements

Investment account statements

Bills from all service providers

Step 2: Identify fees

Highlight every charge that isn't the base service cost

Look for recurring charges you don't recognize

Note fees that have increased over time

Step 3: Research alternatives

Compare fee structures of competitors

Look for fee-free alternatives

Calculate annual cost of current fees

Step 4: Negotiate or switch

Call current providers to negotiate fee waivers

Cancel unnecessary services

Switch to lower-fee alternatives

The Power of Saying No

Default to "no" on add-ons: Extended warranties, insurance, premium features

Question every fee: "What is this for? Can it be waived? What are my alternatives?"

Don't accept "policy": Policies can often be overridden by managers

Be willing to walk away: The best negotiating position is not needing the service

Tools and Resources

Fee tracking apps: Personal Capital, Rocket Money for subscription management

Virtual credit cards: Privacy.com, IronVest for trial management

Price comparison sites: For utilities, insurance, banking services

Consumer protection sites: Clark.com, NerdWallet for fee information

My Personal Fee Horror Stories

The Gym That Wouldn't Die

I signed up for a gym membership with a "simple" month-to-month contract. When I moved out of state and tried to cancel:

Required a 30-day written notice on their “special form”

Had to cancel in person at the original location (1,500 miles away)

Given “free” personal training sessions for three months that automatically converted into paid sessions (unless you filled out the special 30-day cancellation form)

Called me relentlessly (monthly at least) for 5+ years to get me back as a customer even though I repeatedly told them I had left the state!

The Cable Company Shell Game

Signed up for "internet only" service advertised at $39.99/month. Final bill breakdown:

Internet service: $39.99

Equipment rental: $10.99

Installation fee: $99.99

Activation fee: $39.99

Taxes and fees: $18.47

Advertised: $39.99/month

Actual first month: $209.43

The Investment Fee Revelation

I discovered my grandmother’s financial advisory firm was charging ~2.4% annually in fees across expense ratios and administrative costs. On a $100,000 balance, that's $2,400/year.

We moved her to Charles Schwab with index funds at using 0.1% expense ratios and below. (Note: I don’t use Schwab personally, though I have been pleased with their service.)

Annual savings: $2,400 (which compounds for decades)

Making It Systematic

Monthly Tasks

Review bank and credit card statements for new fees

Check subscription charges against services actually used

Monitor investment account fees and performance

Quarterly Tasks

Audit all recurring subscriptions

Shop insurance rates and service providers

Review and negotiate annual fees

Annual Tasks

Complete fee audit across all accounts and services

Calculate total annual fees paid and set reduction goals

Research new fee-free alternatives for major services

The FI Connection

Hidden fees are the enemy of financial independence because:

They're pure waste: No value received for money spent

They compound: Small fees become large amounts over time

They're avoidable: With attention and effort, most can be eliminated

They teach bad habits: Accepting fees trains you to accept higher costs everywhere

Every fee you eliminate is money that can work toward your freedom instead of corporate profits.

Red Flags to Watch For

"Free" anything that requires payment info Prices ending in .95 or .99 (often excludes taxes and fees)

"Starting at" pricing (base price excludes necessary features)

Complex fee structures (designed to confuse)

Difficult cancellation policies (designed to trap customers)

Automatic renewals (especially for annual terms)

Add-ons selected by default (opt-out instead of opt-in)

The Bottom Line

Companies have entire departments dedicated to extracting maximum revenue through fees. They're professional fee collectors. You need to become a professional fee avoider.

The key principles:

Read everything before agreeing to any service

Question every fee and demand explanations

Negotiate aggressively or walk away

Audit regularly to catch new fees quickly

Choose providers based on total cost, not advertised prices

Remember: Every dollar spent on fees is a dollar that can't work toward your financial independence. Treat fee avoidance as seriously as you treat investing.

Next time, we'll explore healthcare considerations for early retirement, addressing one of the biggest concerns people have about leaving employer-provided benefits.

Until then, your homework: Conduct a fee audit on one category this week. Pick banking, subscriptions, or insurance and calculate how much you're paying in fees annually. You might be shocked by the results.

Here's to keeping your money working for you,

Max

Remember: If a company makes it hard to cancel, they're probably not providing value worth keeping. Vote with your wallet and find providers who compete on service, not on making it difficult to leave.