Unlocking Your Retirement Accounts Before 59½

The Roth Conversion Ladder and Other Strategies

Most people believe their 401(k) and IRA money is locked away until age 59½. That belief stops some people from pursuing early retirement at all. It isn’t true, but the escape routes require planning years in advance. Ignore this topic and you may find yourself financially independent on paper while unable to access your own money without a penalty.

This post explains exactly how to get to your retirement funds early, legally, and in some cases, with minimal tax impact. We will cover five strategies, including the one most FIRE people rely on: the Roth conversion ladder.

First: Understanding the Three Buckets

Before diving into early withdrawal strategies, you need to understand where your money sits. Retirement savers typically have three types of accounts, each with different rules:

Taxable brokerage: No contribution limits, no age restrictions on withdrawals. You pay capital gains tax when you sell, but you can access the money anytime. This is the simplest bucket.

Tax-deferred accounts (Traditional 401(k), Traditional IRA): You got a tax deduction going in. The IRS wants its cut on the way out. Withdraw before 59½ and you owe ordinary income tax plus a 10% penalty. These are the accounts that create the problem.

Roth accounts (Roth IRA, Roth 401(k)): Contributions were made with after-tax dollars. Qualified withdrawals are tax-free. But the rules around early access are more nuanced than most people realize.

People who followed conventional savings advice of maximizing the 401(k) first for the tax deduction, then funding an IRA often arrive at early retirement with the bulk of their wealth in tax-deferred accounts. That’s not a mistake; those accounts have annual limits, and any savings above the limit naturally ends up in taxable accounts. But it does mean you need a plan to access the tax-deferred money before 59½ without getting hit with a 10% penalty on top of ordinary income taxes.

Option 1: Taxable Brokerage: The Simplest Solution

If you have significant assets in a taxable brokerage account, congratulations: you have no early withdrawal problem. Sell shares, pay capital gains tax at the applicable rate (0%, 15%, or 20% depending on your income), and spend the proceeds. No penalty, no age restriction, no complicated rules.

The catch is that most people who followed the standard advice of maxing tax-deferred accounts first don’t have enough in taxable accounts to fund a long early retirement. If you retire at 50 with $1 million in a 401(k) and $50,000 in a brokerage, the taxable account runs out quickly. You need a bridge strategy.

The taxable brokerage is also the key to making the Roth conversion ladder work, as you’ll see below. The two strategies work together.

Note: I’m not saying to ignore IRAs and 401ks in favor of standard brokerage accounts. The tax advantages are real and you should use them. I’m just saying it creates a problem for early retirement.

Option 2: Roth Contributions: Already Accessible

Here is something that surprises most people: you can withdraw your Roth IRA contributions at any time, at any age, with no tax and no penalty. The 10% penalty only applies to earnings, not to the money you originally put in.

Example: You contributed $50,000 to a Roth IRA over the years and it has grown to $80,000. You can withdraw $50,000 (your contributions) at age 40 with no penalty. The $30,000 in earnings must stay until 59½ (or until the 5-year rule is satisfied, more on that shortly).

This is often overlooked as an early retirement strategy. If you have been funding a Roth IRA consistently, you may have a meaningful pool of penalty-free money available right now.

Important distinction: this only applies to direct Roth IRA contributions. Money that was converted from a traditional IRA or 401(k) into a Roth follows different rules. That’s where the conversion ladder comes in.

Option 3: The Roth Conversion Ladder: The Main Strategy

The Roth conversion ladder is the primary tool most early retirees use to access tax-deferred money before 59½ without penalty. It requires patience (five years of it), but it is legal, effective, and can be done in a very tax-efficient way.

What Is a Roth Conversion?

A Roth conversion moves money from a traditional IRA or 401(k) into a Roth IRA. You pay ordinary income tax on the converted amount in the year of conversion because you never paid tax on it going in. After that, the money lives in the Roth and grows tax-free.

There is no limit on how much you can convert in a year, and there are no income restrictions. Anyone can do a Roth conversion.

The Two 5-Year Rules Explained Clearly

This is where most explanations fail. There are two separate 5-year rules for Roth accounts, and they apply to different things. Confusing them is an expensive mistake.

5-Year Rule #1: The Roth IRA account itself.

Your Roth IRA must have been open for at least 5 years before earnings can be withdrawn tax-free. This clock starts on January 1 of the year you made your first contribution to any Roth IRA. It is a one-time clock. Once satisfied, it applies to all your Roth IRAs forever. If you opened a Roth IRA at any point in your working years, you likely already satisfy this rule.

5-Year Rule #2: Each individual conversion.

This is the one that matters for the ladder. Every time you convert money from a traditional IRA to a Roth IRA, that specific conversion must sit in the Roth for 5 years before you can withdraw it penalty-free. Each conversion starts its own 5-year clock on January 1 of the conversion year. This rule applies regardless of your age, as long as you are under 59½.

So if you convert $40,000 in 2025, you can withdraw that $40,000 penalty-free on January 1, 2030, five calendar years later. Convert another $40,000 in 2026, and that becomes available January 1, 2031.

The IRS counts calendar years, not 365-day periods. A conversion made on December 31, 2025 still starts its clock on January 1, 2025, meaning it becomes available January 1, 2030, not January 1, 2031. Converting in early January gives you an extra year of growth for the same wait.

How the Ladder Works

The mechanics are simple: convert a chunk of traditional IRA money to a Roth IRA each year, pay the income tax now, and wait five years. Then each year’s conversion becomes accessible in sequence (hence the “ladder”).

The challenge is the first five years. You have converted money into your Roth, but you cannot touch those specific converted funds yet. You need something else to live on during that waiting period. That is where the taxable brokerage account or existing Roth contributions serve as the bridge.

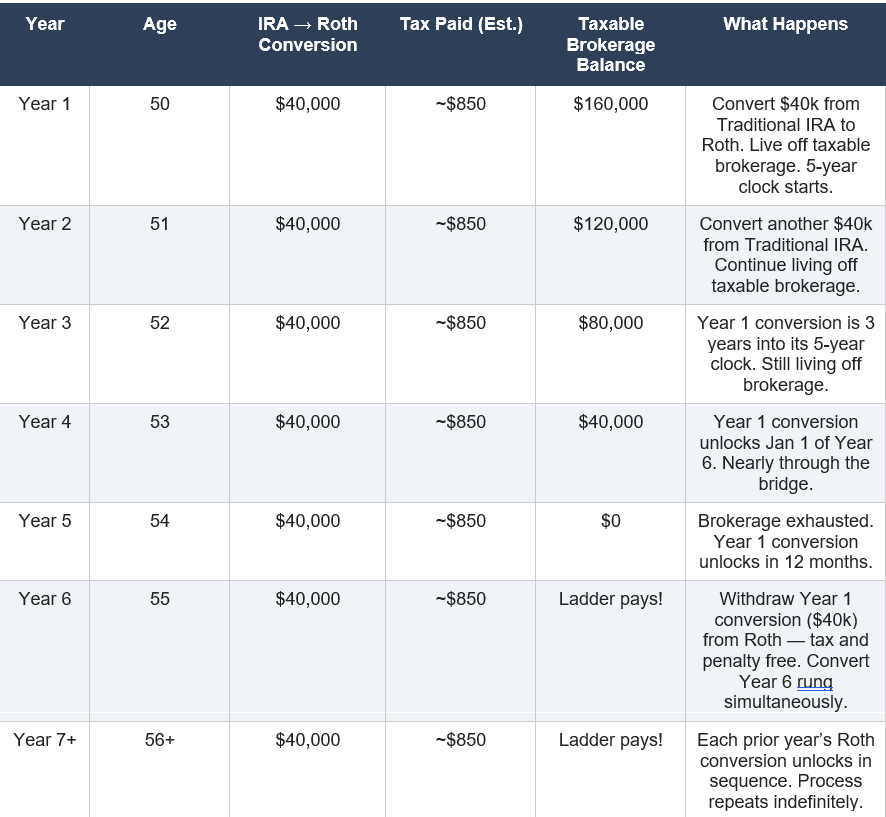

Example: Will and Jordan

Will and Jordan are both 50. They retire with $800,000 in traditional IRA and 401(k) accounts and $200,000 in a taxable brokerage. They need ~$39,000 per year to live on. Here is how they build the ladder.

Each year they convert $40,000 from their traditional IRA to a Roth IRA. Why $40,000? The 2025 standard deduction for married filing jointly is $31,500. Subtract that from the $40,000 conversion and they have $8,500 of taxable income. That entire amount sits in the 10% bracket, meaning they owe roughly $850 in federal income tax on the conversion. They are moving money from tax-deferred to tax-free at an effective rate just above 2% on the gross conversion amount. This is far lower than they paid during their working years and also why tax-deferred accounts can be so useful.

By year 6, the ladder is self-sustaining. They withdraw the previous year’s conversion from the Roth (tax and penalty free) while converting a new rung. The $200,000 taxable brokerage funded the bridge period. The traditional IRA continues to shrink at a controlled, low-tax rate.

At 59½, the penalty rules disappear entirely. By then, they will have converted a large portion of the traditional IRA at historically low tax rates, reducing future required minimum distributions (RMDs) and leaving a larger tax-free Roth balance.

The ACA Subsidy Angle

One important consideration is healthcare subsidies. Early retirees with no wage income often have very low modified adjusted gross income (MAGI). If that MAGI falls below the federal poverty level (roughly $20,000 for a single person or $27,750 for a couple in 2025), they become ineligible for ACA marketplace subsidies and instead qualify only for Medicaid.

Roth conversions deliberately raise MAGI. Many early retirees use conversions not just for the ladder strategy, but to keep their income high enough to remain eligible for ACA marketplace coverage and premium tax credits. This is a case where paying some tax voluntarily is actually the financially correct move. (In most states, but not all, marketplace coverage is more widely accepted than Medicaid.)

Note: The enhanced ACA subsidies that were in place from 2021 through 2025 have expired. Subsidy calculations for 2026 are based on the pre-enhancement formula, which is less generous. If you are planning around ACA subsidies, verify current rules with a tax professional, as this policy area remains subject to change.

Option 4: Rule of 55

If you leave your job at age 55 or older, you can take penalty-free distributions from your employer’s 401(k) plan. (The one from the job you just left.) This is called the Rule of 55, and it requires no conversion, no waiting period, and no complicated mechanics.

The key requirements:

• You must leave your employer (voluntarily or through layoff) in the calendar year you turn 55 or later.

• The money must stay in that employer’s plan. If you roll it to an IRA before taking distributions, you lose the Rule of 55 benefit.

• It only applies to the 401(k) from the employer you left at 55+. IRAs and 401(k)s from prior jobs do not qualify.

For someone planning to retire at exactly 55, this can be a clean and simple solution. You still owe ordinary income tax on distributions, but the 10% penalty disappears. If you are retiring earlier than 55, you will need one of the other strategies to bridge the gap.

Option 5: SEPP / 72(t) (Use With Caution)

Section 72(t) of the tax code allows you to take substantially equal periodic payments (SEPP) from your IRA or 401(k) before 59½ without the 10% penalty. You choose one of three IRS-approved calculation methods, and the resulting payment schedule must be followed without deviation for at least five years or until you reach 59½, whichever is longer.

The problem is the inflexibility. If you need more money one year, or if your circumstances change, you cannot deviate from the schedule without triggering the penalty retroactively on every distribution you have already taken, plus interest. This has ruined people financially. A medical emergency, a one-time large expense, or simply changing your mind about how much you need can turn a legal strategy into a tax disaster.

SEPP is worth knowing about as a last resort. For most early retirees with a taxable brokerage or the ability to do Roth conversions, there is a better option. If you believe SEPP might apply to your situation, work with a qualified tax professional before starting.

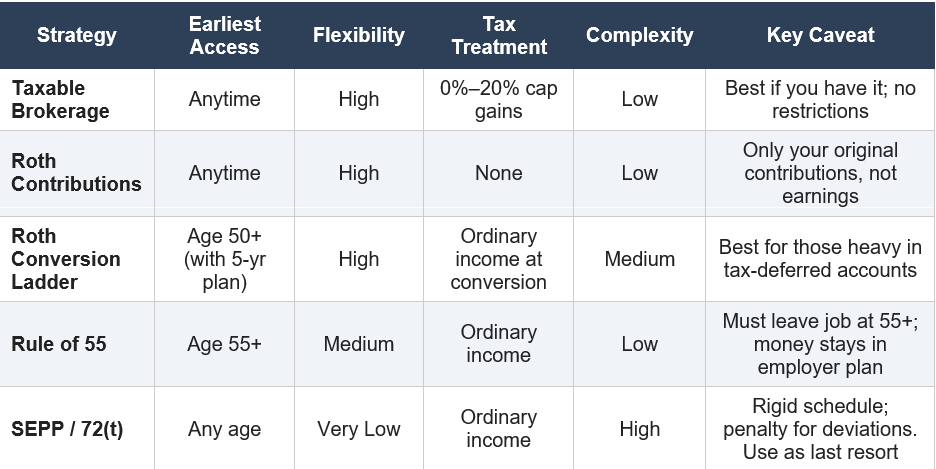

Choosing Your Strategy: A Simple Decision Framework

Not everyone needs the Roth conversion ladder. Your account mix determines which approach makes sense:

Heavy taxable brokerage (40%+ of assets): Live off the taxable account. The ladder may still be useful for managing future RMDs and ACA subsidies, but it is not your primary income source.

Mix of taxable and tax-deferred: Use the taxable account as your bridge while building the Roth ladder from the tax-deferred portion. This is the most common early retiree scenario.

Mostly tax-deferred: The ladder is essential. Start conversions as early as possible, ideally 5 years before you expect to need the money.

Retiring at exactly 55+: The Rule of 55 may be simpler for your current employer plan. Consider a hybrid approach.

The Planning Implication for Accumulators

If you are still building wealth, the most important takeaway is this: your account mix today determines your options at retirement. The Roth conversion ladder requires a bridge, typically 5 years of living expenses in a taxable account or Roth contributions. If you arrive at early retirement with 100% of your assets in tax-deferred accounts and nothing in taxable or Roth, you have a problem that takes years to solve and costs real money in taxes along the way.

The conventional advice to always max your 401(k) first is reasonable, but it is not the complete picture for early retirees. Maxing your 401(k), then your IRA, and then investing additional savings in a taxable brokerage is the path that preserves the most flexibility. The 401(k) and IRA give you the tax deduction while you’re earning. The taxable brokerage gives you the bridge when you stop.

One more note on timing: conversions are most efficient when your income is low. The year you retire (when you have half a year of salary plus no income for the second half) is often an excellent year to start converting. So is any year where income happens to be lower than usual. Do not wait until you need the money. Start the 5-year clock as early as your situation allows.

A Personal Note

I do Roth conversions every year. What I do not do is use the ladder for withdrawals. My situation is different: I have enough in taxable brokerage accounts to fund my spending without touching converted Roth funds, so I let the Roth grow tax-free as long as possible. That is the right call for my circumstances.

But for someone who followed the more common path of maximizing tax-deferred accounts throughout a career with limited taxable savings, the Roth conversion ladder is not optional. It is the primary mechanism for accessing your own money without paying a penalty for retiring too early.

Understand the strategy. Build the bridge. Start the clock before you need it.

Summary Comparison Table

All figures based on 2025 tax law. Tax law changes frequently. Verify current brackets, standard deductions, and ACA rules before executing any strategy. Consult a qualified tax professional for your specific situation.

Until next time,

Max